We know what’s coming and we are prepared.

🛢⛽️ Global oil inventories are heading toward RECORD LOWS:

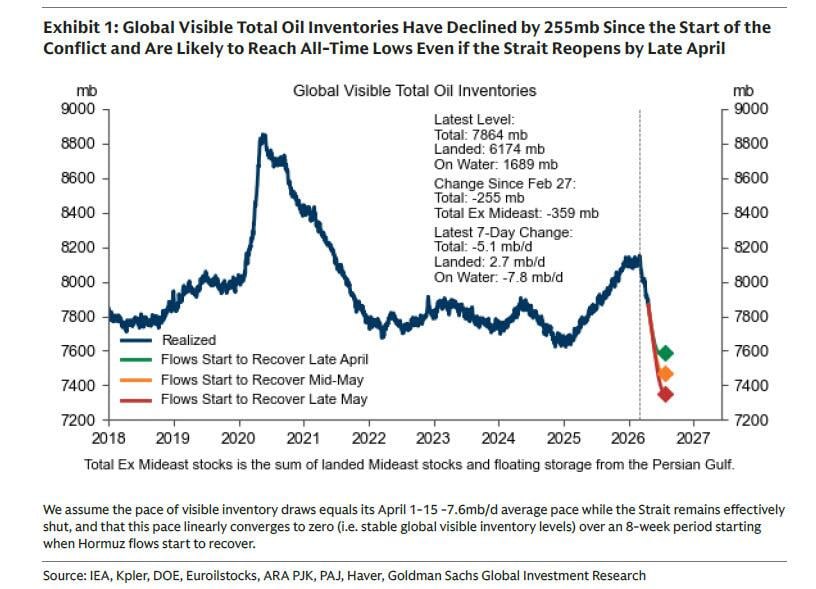

Global visible oil inventories have fallen -255 million barrels since the start of the conflict on February 27, to 7,864 million barrels.

Total estimated oil draws, including non-OECD refined products storage, have accelerated to 10.9 million barrels per day in April, the largest monthly draws on record since 2017.

Cumulative estimated draws since the start of the war now stand at 474 million barrels, with Hormuz flows holding at ~10% of normal, or 2.0 million barrels per day.

Meanwhile, even in an optimistic scenario where Strait of Hormuz flows begin recovering by late April, it is unlikely to prevent global visible inventories from reaching all-time lows, according to Goldman Sachs.

As inventories keep falling, physical oil markets are likely to require sharply higher prices for immediate delivery, since buyers cannot wait months for cheaper futures delivery when stocks are running critically low.

Goldman also warns that inventories cannot keep falling forever, and once they approach the minimum level needed to keep global supply chains running, the only way the market can rebalance is by destroying demand.

The global oil buffer is disappearing fast, which means oil prices are set to rise further.

🔗 Global Markets Investor

🇺🇸🇮🇷⚡️- “U.S. Central Command (CENTCOM) completed another round of strikes against Iran at 9 p.m. ET, July 20.

U.S. forces struck Iranian military command centers, maritime capabilities, missile and drone launch sites, and air defense systems to degrade Iran's ability to continue attacking commercial vessels flowing through the Strait of Hormuz.

Commercial vessel transits through the vital international maritime corridor continue. Since early May, CENTCOM forces have helped facilitate the transit of approximately 900 commercial vessels and 450 million barrels of crude oil.

American forces remain postured and prepared to hold Iran accountable for unwarranted aggression toward civilian mariners seeking to freely and openly transit the strait.” - U.S. Central Command.

“This is insane!” — A new vaccine is on the market called VAXELIS lt has 6 VACCINES in ONE SHOT for 6-WEEK-OLD BABIES...6 Infants Died In Trials.

How can this be allowed to happen ?

Dr. Jeff Barke

Mike

Subscribe: The Lost Past ⏳

I found a hidden channel: "Banned Truth" check it out before it disappears!

🌆 Market News Digest

[2026-07-19 17:00–2026-07-20 16:30 EST]

🔥 Top Stories

• U.S.-Iran conflict escalates — fresh U.S. strikes, Iranian retaliation, and talks/ceasefire chatter keep markets on edge

• Oil surges on Hormuz risk — Brent topped $90 intraday, WTI near $83, with tanker incidents and Saudi/Hormuz shipping threats

• Trump escalates pressure on Iran — says Iran will “pay” for U.S. deaths; U.S. adds aircraft and signals next campaign phase

• Canada CPI cools — headline CPI eased to 2.8% y/y, supporting easier BoC path and denting CAD

• UK government reset — Starmer resigned; Burnham took over with a reshuffled cabinet, pledging fiscal rules but more flexibility

⛽ Oil & Energy

• Tankers hit / shipping disrupted — fires, explosions and drone threats in Strait of Hormuz, Bahrain, Kuwait and off Oman

• Chevron shuts Petronius output — Gulf platform shut-in as storm risk adds to energy supply worries

• CPC oil loadings suspended — attacks on tankers halt Kazakhstan ...

⛽️ While the price of crude oil is still below the prices seen during the peak of the 3rd Gulf War fighting, diesel prices on the other hand are surging and surpassed their peak in May.

Diesel is the most important fuel for the global economy, widely used in agriculture to fuel tractors and combine-harvesters.

@CIG_telegram